Implementation of 5-factor Fama French Model

This project contains implementation of five factor Fama French model + jupyter notebook for exploratory analysis.

Risk Factor

Certain characteristic of economy (Inflation/GDP) or stock market itself (S&P 500)

Factor Model

Factor model uses movements in risk factors to explains portfolio returns

Questions which factor investing answers

- Why different asset have systematically lower or higher average returns?

- How to manage the asset portfolio with the underlying risks in mind?

- How to benefit of our ability to bear specific types of risks to generate returns?

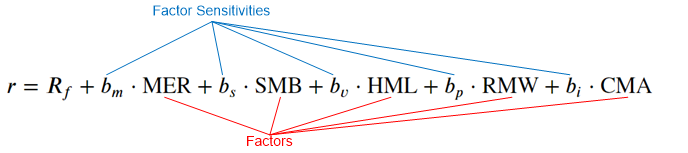

Fama-French Model

Assumes linear relationship between empirical factors and stock returns:

- Market Factor (MER)

- Size Factor (SMB)

- Value Factor (HML)

- Profitability Factor (RMW)

- Investment Factor (CMA)

Factors are constructed daily from definitions, as illustrated previously

- They are global for the entire stock market

Factor sensitivities are calibrated using regression

- They represent “reward for taking a specific risk”, which is different for every stock

- Risk/Reward relationship is expected to hold over time

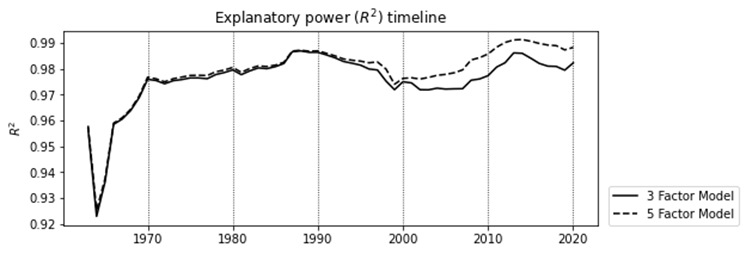

- Objective: maximize the model’s predictive power R2

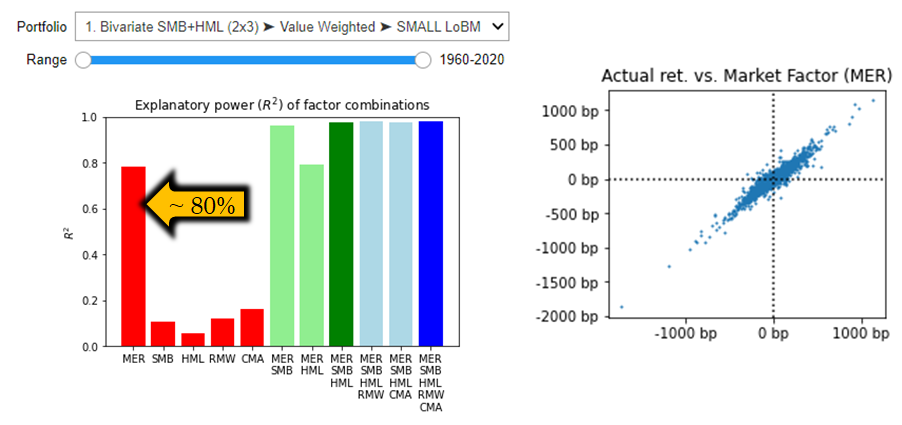

Market Excess Return (MER)

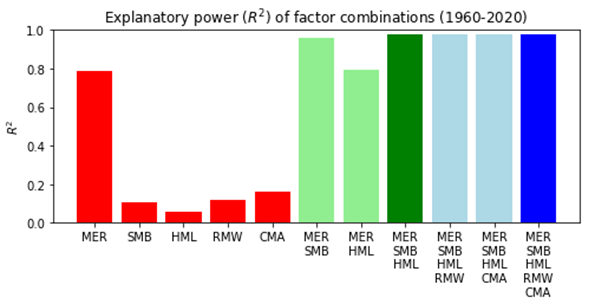

- Market excess return (over RF rate) alone explains around 80% of asset movements

- Daily returns are ~normally distributed

- Relationship between returns of the overall market and returns of selected portfolio

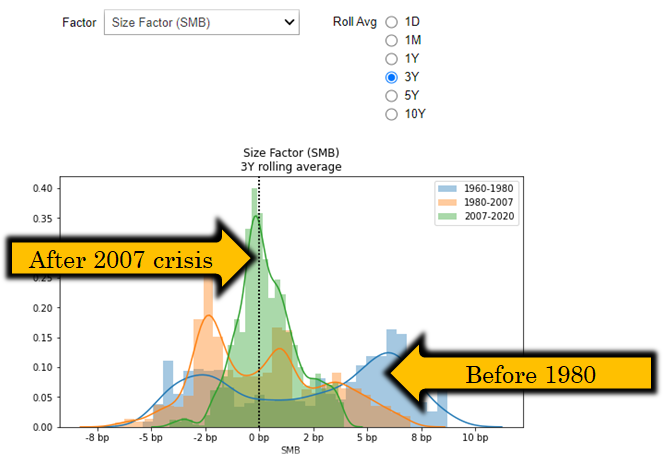

Size (SMB) factor

- Small-cap companies typically bear additional risk premium - was it always the case?

- Python can help you to see that this factor has a different prevalence in different economic regimes

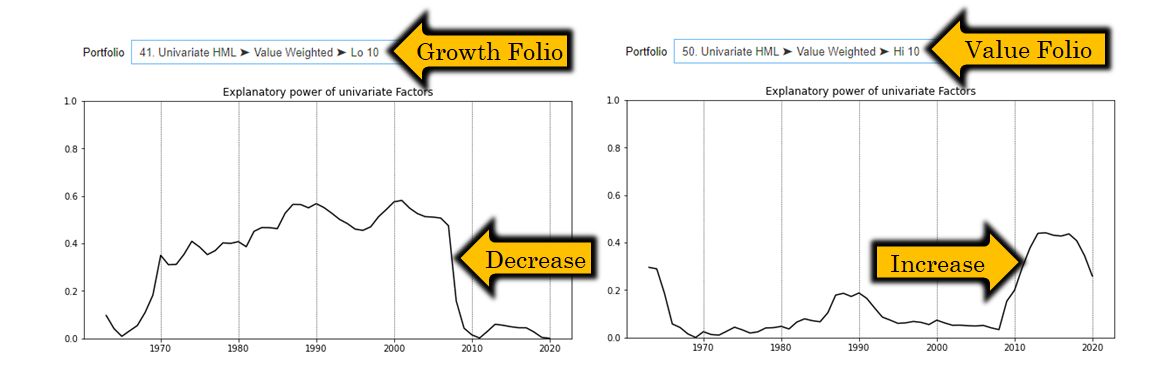

Value (HML) factor

- Value companies trade at higher yields to compensate for lack of growth potential

- Python can help you to see that this factor has different explanatory power in different market situations and on different portfolios (very interesting)

Profitability and investment factors

- Profitability factor> (RMW) to attribute superior returns of companies with robust operating profit margins and strong competitive position among peers

- Investment factor (CMA) to segment companies based on their capital expenditures

- Analysts opinion: High capex structurally associated with growth companies, which puts usefulness of this factor in question

Evaluating 5-factor model

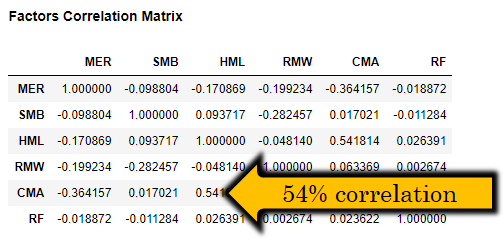

- Analyst opinion: High correlations between risk factors puts usefulness of 5-factor model into question.

- R2 10-20% for RMW, CMA

- 5 factor improvement only by 0.2%

More features and information

- Interactive return attribution

- Time-series analysis

- Portfolio returns and factors loaded from Fama-French data library (https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html)

- Please refer to the blog post http://www.quantandfinancial.com/2020/06/famafrench.html for more details