Decomposing a time series means separating it into its constituent components, which are usually a trend component and an irregular component, and if it is a seasonal time series, a seasonal component. For the TSLA stock information, from the price trend plot figure, we can see that there is not seasonal component inside the data. But this time series data should include a trend component and an irregular component. Decomposing the time series involves trying to separate the time series into these components, that is, estimating the trend component and the irregular component. We will SMA() function to smooth TSLA data. We will choose the different order (n=8 and n=40) to check the trend component. The goal is that we try to smoothed the data with a simple move average.

ARIMA Model

ARIMA (Autoregressive Integrated Moving Average) is a major tool used in time series analysis to attempt to forecast future values of a variable based on its present value. ARIMA(p,d,q) forecasting equation: ARIMA models are, in theory, the most general class of models for forecasting a time series which can be made to be “stationary” by differencing. ARIMA models are defined for stationary time series. Therefore, if you start off with a non-stationary time series, you will first need to ‘difference’ the time series until you obtain a stationary time series. To difference the time series d times to obtain a stationary series, we use the diff() function. Then we will use the A formal ADF test does not reject the null hypothesis of non-stationarity, confirming our visual inspection:

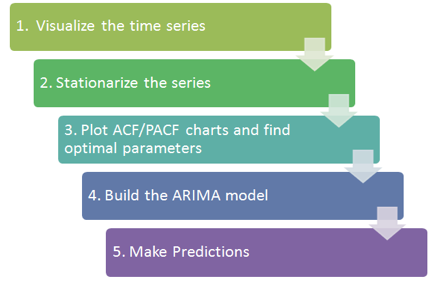

In this section, we use the TESLA stock data as time series. We decompose it and use the HoltWinter exponential smoothing and ARIMA to forecast the future stock price. The basic procedures are as the following figure.

The other thing is we should always to analysis the errors and tune model parameters to achieve the better results.