Objectives

- Develop an interactive dash app in Python with financial data.

- Display the historical performances of quantitative factors in Quant Investing from Fama-French Data Library.

- Introduce various types of portfolio asset allocation strategies and analyze the historical performances and statistics.

Fama-French Quantitative Factors

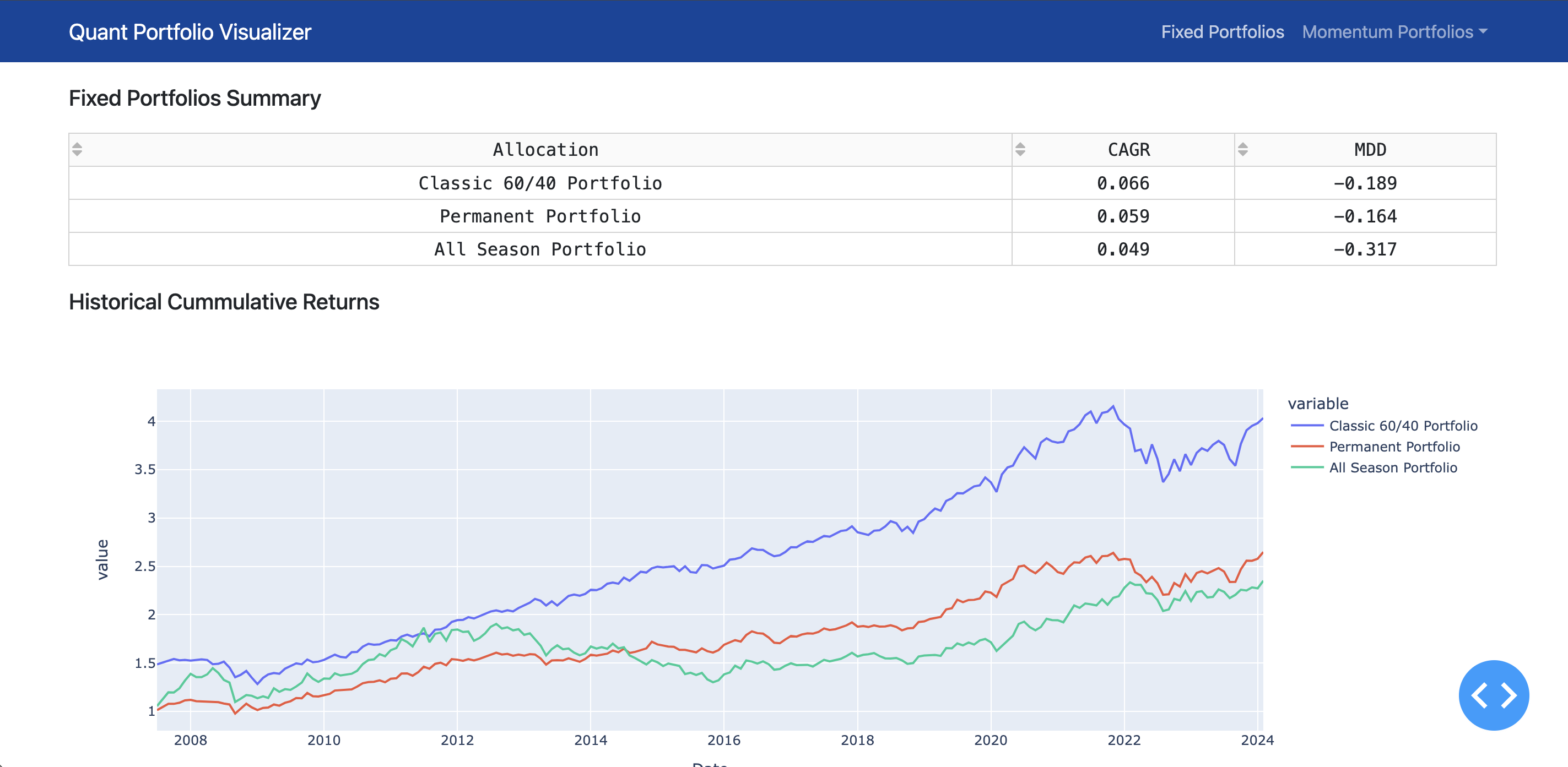

Portfolio Asset Allocation Strategies

- Classic 60% Equities + 40% Bonds Portfolio

- Four Seasons Portfolio

- All Weather Portfolio

- Permanent Portfolio

- Dual Momentum by Gary Antonacci

- Vigilant Asset Allocation (VAA) by Wouter J. Keller

- Defensive Asset Allocation (DAA) by Wouter J. Keller

- Lethargic Asset Allocation (LAA) by Wouter J. Keller

How to Install and Run

- Clone the repo

- Run virtual environment by

source venv/bin/activate

- Run

python src/app.py

- Wait until you see

Dash is running on http://127.0.0.1:8050/ on the console.

Data Source

- Kenneth R. French - Data Library

Demo Screenshot