Canalys' latest report shows that the global personal smart audio device market rebounded strongly in the third quarter of 2024, with shipments approaching 126 million units, a year-on-year increase of 15%. The editor of Downcodes will interpret this report for you, analyzing the driving forces behind market growth and the outstanding performance of each region and brand. This report demonstrates the positive trends in market recovery and growing consumer demand for high-performance audio equipment.

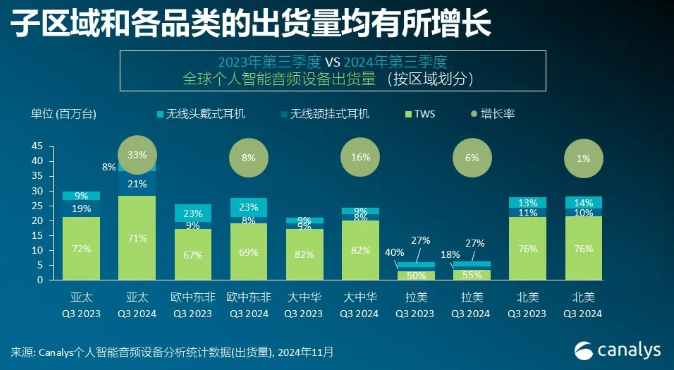

Canalys data shows that in the third quarter of 2024, the global personal smart audio device market ushered in a strong rebound, with total shipments approaching 126 million units, an increase of 15% compared with the same period last year.

This growth trend shows that the market has successfully shaken off the downturn in 2023 and is showing good momentum for continued recovery. All major sub-regions benefited from this general growth, with all major product categories recording double-digit growth in shipments.

Among various markets, India performed particularly well, with shipments increasing by 51%, approximately 9 million units more than in the third quarter of 2023. This growth was mainly driven by a 47% increase in shipments of TWS (True Wireless Stereo) devices. At the same time, driven by brands such as boAt and OnePlus, the shipment growth rate of wireless neck-mounted headphones has reached 65%. In response to growing consumer demand, boAt has relaunched its popular old wireless neckband headphones.

Research shows that devices with active noise cancellation (ANC) function account for 21% of the Indian market. 52% of the OnePlus brand's devices shipped are equipped with ANC functionality, indicating consumers' growing preference for high-performance devices with advanced features.

In addition, the open-back headphone market is also growing significantly in the third quarter of 2024, with shipments almost tripling, which is closely related to the growth trend in the global health and fitness field. The demand for open-type TWS and wireless neck-mounted headphones has surged, accounting for 6% of the overall market. Specialty brands such as Shokz and Sanag have performed particularly well in this area, with Shokz's shipments growing significantly in North America and Western Europe.

Although mainland China still accounts for 59% of the world's share of open-back headphone shipments, Chinese audio equipment brands are actively expanding into international markets. They attract new customers and gain market share by launching entry-level products. As brands gradually gain stable market share, they will face new challenges in improving product quality and innovation in the future.

All in all, the global personal smart audio device market shows a strong recovery trend, and the Indian market growth is particularly significant. Different types of headphone products have achieved growth and demonstrated the competitive landscape of different markets and brands. In the future, product innovation and market expansion will become the key to industry development.