pandas ta

v0.3.14b

يعد التحليل الفني لـ Pandas ( Pandas TA ) مكتبة سهلة الاستخدام تستفيد من حزمة Pandas مع أكثر من 130 مؤشرًا ووظائف المنفعة وأكثر من 60 TA LIB Candlestick. يتم تضمين العديد من المؤشرات شائعة الاستخدام ، مثل: نمط الشمعة ( CDL_Pattern ) ، متوسط متوسط الحركة المتوسط المتحرك ( SMA ) المتوسط المتوسط ( MACD ) ، المتوسط المتحرك الأسي للبدن ( HMA ) ، نطاقات Bollinger ( BBANDS ) ، حجم الموازن ( OBV (OBV) ) ، آرون آند آرون مذبذب ( أرون ) ، الضغط ( الضغط ) وغيرها الكثير .

ملاحظة: يجب تثبيت TA LIB لاستخدام جميع أنماط الشموع. pip install TA-Lib . إذا لم يتم تثبيت TA LIB ، فستتوفر أنماط الشموع المدمجة فقط.

talib=False .ta.stdev(df["close"], length=30, talib=False) .import_dir تحت /pandas_ta/custom.py .ta.tsignals .lookahead=False لتعطيل.يتحقق Pandas TA إذا كان لدى المستخدم بعض حزم التداول الشائعة المثبتة بما في ذلك على سبيل المثال لا الحصر: TA LIB ، Vector BT ، yfinance ... الكثير منها تجريبي ومن المحتمل أن ينكسر حتى يستقر أكثر.

help(ta.ticker) help(ta.yf) والأمثلة أدناه. إصدار pip هو آخر إصدار مستقر. الإصدار: 0.3.14b

$ pip install pandas_taأفضل خيار! الإصدار: 0.3.14b

$ pip install -U git+https://github.com/twopirllc/pandas-taهذا هو نسخة التطوير التي يمكن أن تحتوي على الأخطاء وغيرها من الآثار الجانبية غير المرغوب فيها. استخدام في خطر خاص!

$ pip install -U git+https://github.com/twopirllc/pandas-ta.git@development import pandas as pd

import pandas_ta as ta

df = pd . DataFrame () # Empty DataFrame

# Load data

df = pd . read_csv ( "path/to/symbol.csv" , sep = "," )

# OR if you have yfinance installed

df = df . ta . ticker ( "aapl" )

# VWAP requires the DataFrame index to be a DatetimeIndex.

# Replace "datetime" with the appropriate column from your DataFrame

df . set_index ( pd . DatetimeIndex ( df [ "datetime" ]), inplace = True )

# Calculate Returns and append to the df DataFrame

df . ta . log_return ( cumulative = True , append = True )

df . ta . percent_return ( cumulative = True , append = True )

# New Columns with results

df . columns

# Take a peek

df . tail ()

# vv Continue Post Processing vv تم إعادة ترتيب بعض حجج المؤشر للاتساق. استخدم help(ta.indicator_name) لمزيد من المعلومات أو تقديم طلب سحب لتحسين الوثائق.

import pandas as pd

import pandas_ta as ta

# Create a DataFrame so 'ta' can be used.

df = pd . DataFrame ()

# Help about this, 'ta', extension

help ( df . ta )

# List of all indicators

df . ta . indicators ()

# Help about an indicator such as bbands

help ( ta . bbands ) شكرا لاستخدام Pandas TA !

$ pip install -U git+https://github.com/twopirllc/pandas-taشكرا لك على مساهماتك!

لدى Pandas TA ثلاثة "أنماط" أساسية لمعالجة المؤشرات الفنية لحالة الاستخدام و/أو المتطلبات. هم: قياسي ، امتداد DataFrame ، واستراتيجية Pandas TA . كل مع زيادة مستويات التجريد لسهولة الاستخدام. عندما تصبح أكثر دراية بـ Pandas TA ، قد تصبح بساطة وسرعة استخدام استراتيجية Pandas TA أكثر وضوحًا. علاوة على ذلك ، يمكنك إنشاء مؤشراتك الخاصة من خلال التسلسل أو التكوين. أخيرًا ، يقوم كل مؤشر إما بإرجاع سلسلة أو ملف بيانات بتنسيق Underscore Underscore بغض النظر عن الأناقة.

يمكنك تحديد أعمدة الإدخال صراحة وتعتني بالإخراج.

sma10 = ta.sma(df["Close"], length=10)SMA_10donchiandf = ta.donchian(df["HIGH"], df["low"], lower_length=10, upper_length=15)DC_10_15 وأسماء الأعمدة: DCL_10_15, DCM_10_15, DCU_10_15ema10_ohlc4 = ta.ema(ta.ohlc4(df["Open"], df["High"], df["Low"], df["Close"]), length=10)EMA_10 . إذا لزم الأمر ، فقد تحتاج إلى تسمية ذلك بشكل فريد. سيقوم استدعاء df.ta تلقائيًا بتخفيف OHLCVA إلى OHLCVA : مفتوح ، عالي ، منخفض ، إغلاق ، حجم ، adj_close . بشكل افتراضي ، ستستخدم df.ta OHLCVA لوسائط المؤشر التي تزيل الحاجة إلى تحديد أعمدة الإدخال مباشرة.

sma10 = df.ta.sma(length=10)SMA_10ema10_ohlc4 = df.ta.ema(close=df.ta.ohlc4(), length=10, suffix="OHLC4")EMA_10_OHLC4close=df.ta.ohlc4() .donchiandf = df.ta.donchian(lower_length=10, upper_length=15)DC_10_15 وأسماء الأعمدة: DCL_10_15, DCM_10_15, DCU_10_15 مثل الأمثلة الثلاثة الأخيرة ، ولكن إلحاق النتائج مباشرة إلى DataFrame df .

df.ta.sma(length=10, append=True)df : SMA_10 .df.ta.ema(close=df.ta.ohlc4(append=True), length=10, suffix="OHLC4", append=True)close=df.ta.ohlc4() .df.ta.donchian(lower_length=10, upper_length=15, append=True)df بأسماء الأعمدة: DCL_10_15, DCM_10_15, DCU_10_15 . استراتيجية Pandas TA هي مجموعة محددة من المؤشرات التي تديرها طريقة الاستراتيجية . تستخدم جميع الاستراتيجيات MuleTprocessing إلا عند استخدام معلمة col_names (انظر أدناه). هناك أنواع مختلفة من الاستراتيجيات المدرجة في القسم التالي.

# (1) Create the Strategy

MyStrategy = ta . Strategy (

name = "DCSMA10" ,

ta = [

{ "kind" : "ohlc4" },

{ "kind" : "sma" , "length" : 10 },

{ "kind" : "donchian" , "lower_length" : 10 , "upper_length" : 15 },

{ "kind" : "ema" , "close" : "OHLC4" , "length" : 10 , "suffix" : "OHLC4" },

]

)

# (2) Run the Strategy

df . ta . strategy ( MyStrategy , ** kwargs )تعد فئة الإستراتيجية طريقة بسيطة لتسمية مؤشرات TA المفضلة لديك وتجميعها باستخدام فئة بيانات . يأتي Pandas TA مع استراتيجيتين أساسيتين تم تصميمه مسبقًا لمساعدتك في البدء: Allstrategy و Commonstrate . يمكن أن تكون الإستراتيجية بسيطة مثل Commonstrategy أو معقدة حسب الحاجة باستخدام التكوين/التسلسل.

df .راجع أمثلة استراتيجية Pandas TA لأمثلة بما في ذلك تكوين المؤشر/التسلسل .

{"kind": "indicator name"} . تذكر أن تتحقق من الإملاء. # Running the Builtin CommonStrategy as mentioned above

df . ta . strategy ( ta . CommonStrategy )

# The Default Strategy is the ta.AllStrategy. The following are equivalent:

df . ta . strategy ()

df . ta . strategy ( "All" )

df . ta . strategy ( ta . AllStrategy ) # List of indicator categories

df . ta . categories

# Running a Categorical Strategy only requires the Category name

df . ta . strategy ( "Momentum" ) # Default values for all Momentum indicators

df . ta . strategy ( "overlap" , length = 42 ) # Override all Overlap 'length' attributes # Create your own Custom Strategy

CustomStrategy = ta . Strategy (

name = "Momo and Volatility" ,

description = "SMA 50,200, BBANDS, RSI, MACD and Volume SMA 20" ,

ta = [

{ "kind" : "sma" , "length" : 50 },

{ "kind" : "sma" , "length" : 200 },

{ "kind" : "bbands" , "length" : 20 },

{ "kind" : "rsi" },

{ "kind" : "macd" , "fast" : 8 , "slow" : 21 },

{ "kind" : "sma" , "close" : "volume" , "length" : 20 , "prefix" : "VOLUME" },

]

)

# To run your "Custom Strategy"

df . ta . strategy ( CustomStrategy ) تستخدم طريقة استراتيجية Pandas TA المعالجة المتعددة لمعالجة المؤشرات بالجملة لجميع أنواع الاستراتيجية باستثناء واحد! عند استخدام معلمة col_names لإعادة تسمية الأعمدة (العمود) الناتجة ، سيتم تشغيل المؤشرات في ta بالترتيب.

# VWAP requires the DataFrame index to be a DatetimeIndex.

# * Replace "datetime" with the appropriate column from your DataFrame

df . set_index ( pd . DatetimeIndex ( df [ "datetime" ]), inplace = True )

# Runs and appends all indicators to the current DataFrame by default

# The resultant DataFrame will be large.

df . ta . strategy ()

# Or the string "all"

df . ta . strategy ( "all" )

# Or the ta.AllStrategy

df . ta . strategy ( ta . AllStrategy )

# Use verbose if you want to make sure it is running.

df . ta . strategy ( verbose = True )

# Use timed if you want to see how long it takes to run.

df . ta . strategy ( timed = True )

# Choose the number of cores to use. Default is all available cores.

# For no multiprocessing, set this value to 0.

df . ta . cores = 4

# Maybe you do not want certain indicators.

# Just exclude (a list of) them.

df . ta . strategy ( exclude = [ "bop" , "mom" , "percent_return" , "wcp" , "pvi" ], verbose = True )

# Perhaps you want to use different values for indicators.

# This will run ALL indicators that have fast or slow as parameters.

# Check your results and exclude as necessary.

df . ta . strategy ( fast = 10 , slow = 50 , verbose = True )

# Sanity check. Make sure all the columns are there

df . columns تذكر أن هذه لن تستخدم المعالجة المتعددة

NonMPStrategy = ta . Strategy (

name = "EMAs, BBs, and MACD" ,

description = "Non Multiprocessing Strategy by rename Columns" ,

ta = [

{ "kind" : "ema" , "length" : 8 },

{ "kind" : "ema" , "length" : 21 },

{ "kind" : "bbands" , "length" : 20 , "col_names" : ( "BBL" , "BBM" , "BBU" )},

{ "kind" : "macd" , "fast" : 8 , "slow" : 21 , "col_names" : ( "MACD" , "MACD_H" , "MACD_S" )}

]

)

# Run it

df . ta . strategy ( NonMPStrategy ) # Set ta to default to an adjusted column, 'adj_close', overriding default 'close'.

df . ta . adjusted = "adj_close"

df . ta . sma ( length = 10 , append = True )

# To reset back to 'close', set adjusted back to None.

df . ta . adjusted = None # List of Pandas TA categories.

df . ta . categories # Set the number of cores to use for strategy multiprocessing

# Defaults to the number of cpus you have.

df . ta . cores = 4

# Set the number of cores to 0 for no multiprocessing.

df . ta . cores = 0

# Returns the number of cores you set or your default number of cpus.

df . ta . cores # The 'datetime_ordered' property returns True if the DataFrame

# index is of Pandas datetime64 and df.index[0] < df.index[-1].

# Otherwise it returns False.

df . ta . datetime_ordered # Sets the Exchange to use when calculating the last_run property. Default: "NYSE"

df . ta . exchange

# Set the Exchange to use.

# Available Exchanges: "ASX", "BMF", "DIFX", "FWB", "HKE", "JSE", "LSE", "NSE", "NYSE", "NZSX", "RTS", "SGX", "SSE", "TSE", "TSX"

df . ta . exchange = "LSE" # Returns the time Pandas TA was last run as a string.

df . ta . last_run # The 'reverse' is a helper property that returns the DataFrame

# in reverse order.

df . ta . reverse # Applying a prefix to the name of an indicator.

prehl2 = df . ta . hl2 ( prefix = "pre" )

print ( prehl2 . name ) # "pre_HL2"

# Applying a suffix to the name of an indicator.

endhl2 = df . ta . hl2 ( suffix = "post" )

print ( endhl2 . name ) # "HL2_post"

# Applying a prefix and suffix to the name of an indicator.

bothhl2 = df . ta . hl2 ( prefix = "pre" , suffix = "post" )

print ( bothhl2 . name ) # "pre_HL2_post" # Returns the time range of the DataFrame as a float.

# By default, it returns the time in "years"

df . ta . time_range

# Available time_ranges include: "years", "months", "weeks", "days", "hours", "minutes". "seconds"

df . ta . time_range = "days"

df . ta . time_range # prints DataFrame time in "days" as float # Sets the DataFrame index to UTC format.

df . ta . to_utc import numpy as np

# Add constant '1' to the DataFrame

df . ta . constants ( True , [ 1 ])

# Remove constant '1' to the DataFrame

df . ta . constants ( False , [ 1 ])

# Adding constants for charting

import numpy as np

chart_lines = np . append ( np . arange ( - 4 , 5 , 1 ), np . arange ( - 100 , 110 , 10 ))

df . ta . constants ( True , chart_lines )

# Removing some constants from the DataFrame

df . ta . constants ( False , np . array ([ - 60 , - 40 , 40 , 60 ])) # Prints the indicators and utility functions

df . ta . indicators ()

# Returns a list of indicators and utility functions

ind_list = df . ta . indicators ( as_list = True )

# Prints the indicators and utility functions that are not in the excluded list

df . ta . indicators ( exclude = [ "cg" , "pgo" , "ui" ])

# Returns a list of the indicators and utility functions that are not in the excluded list

smaller_list = df . ta . indicators ( exclude = [ "cg" , "pgo" , "ui" ], as_list = True ) # Download Chart history using yfinance. (pip install yfinance) https://github.com/ranaroussi/yfinance

# It uses the same keyword arguments as yfinance (excluding start and end)

df = df . ta . ticker ( "aapl" ) # Default ticker is "SPY"

# Period is used instead of start/end

# Valid periods: 1d,5d,1mo,3mo,6mo,1y,2y,5y,10y,ytd,max

# Default: "max"

df = df . ta . ticker ( "aapl" , period = "1y" ) # Gets this past year

# History by Interval by interval (including intraday if period < 60 days)

# Valid intervals: 1m,2m,5m,15m,30m,60m,90m,1h,1d,5d,1wk,1mo,3mo

# Default: "1d"

df = df . ta . ticker ( "aapl" , period = "1y" , interval = "1wk" ) # Gets this past year in weeks

df = df . ta . ticker ( "aapl" , period = "1mo" , interval = "1h" ) # Gets this past month in hours

# BUT WAIT!! THERE'S MORE!!

help ( ta . yf ) الأنماط غير الجريئة ، تتطلب تثبيت ta-lib: pip install TA-Lib

# Get all candle patterns (This is the default behaviour)

df = df . ta . cdl_pattern ( name = "all" )

# Get only one pattern

df = df . ta . cdl_pattern ( name = "doji" )

# Get some patterns

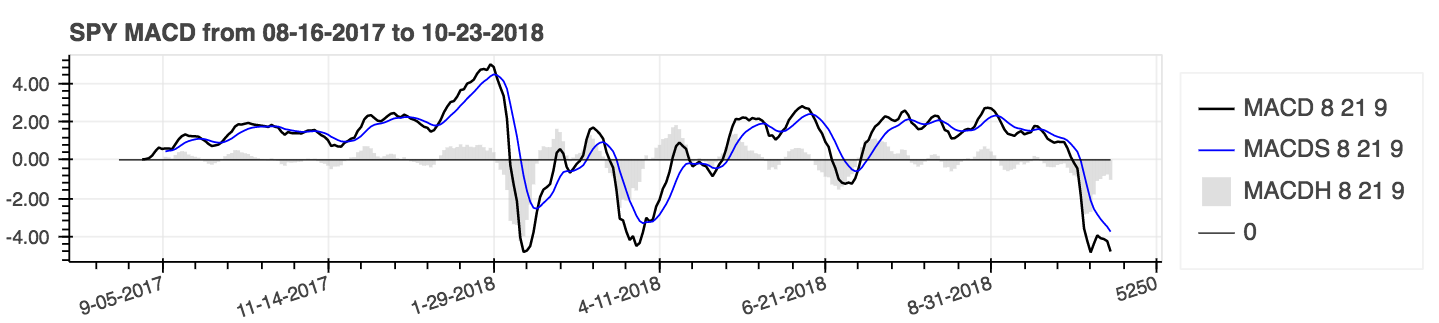

df = df . ta . cdl_pattern ( name = [ "doji" , "inside" ])ta.linreg(series, r=True)lazybear=Truedf.ta.strategy() .| تباعد التقارب المتوسط المتحرك (MACD) |

|---|

|

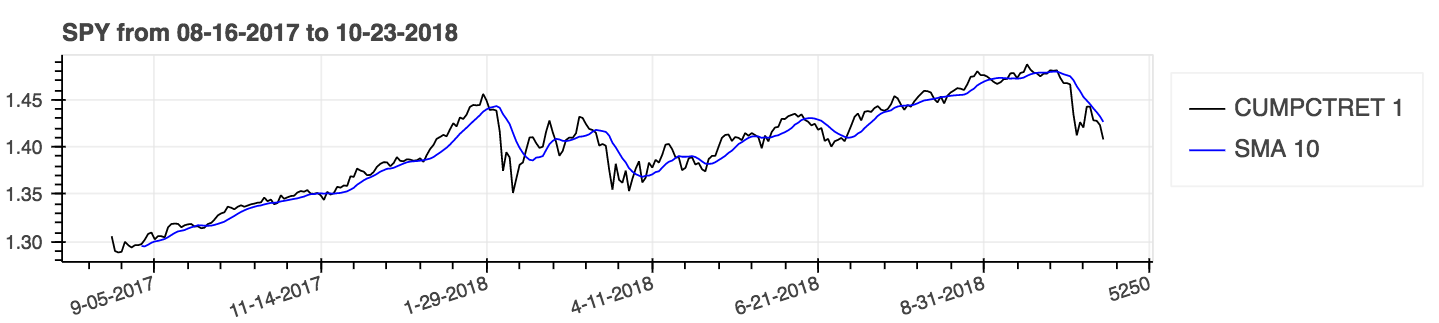

help(ta.ichimoku) .lookahead=False يسقط عمود CHIKOU SPAN لمنع تسرب البيانات المحتمل.| متوسطات الحركة البسيطة (SMA) و Bollinger Bands (Bbands) |

|---|

|

استخدم المعلمة: تراكمية = صواب للنتائج التراكمية.

| عائد في المئة (تراكمي) مع متوسط متحرك بسيط (SMA) |

|---|

|

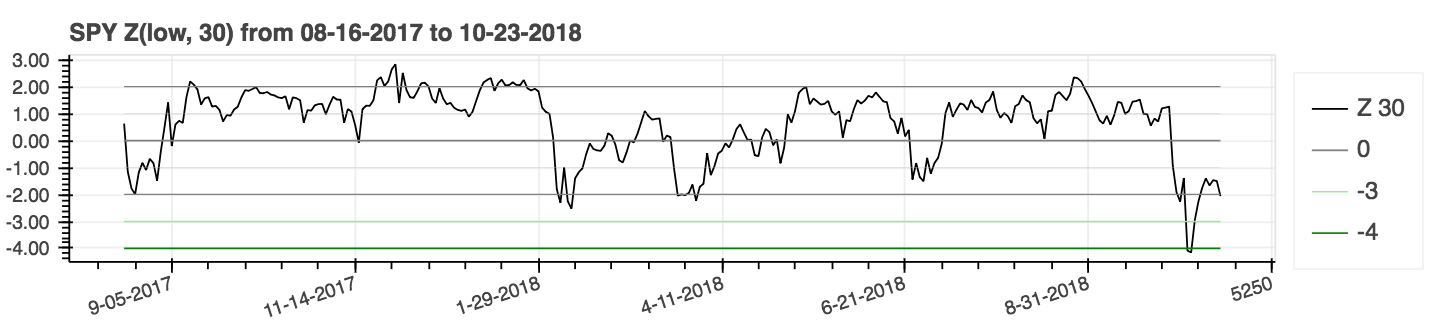

| Z النتيجة |

|---|

|

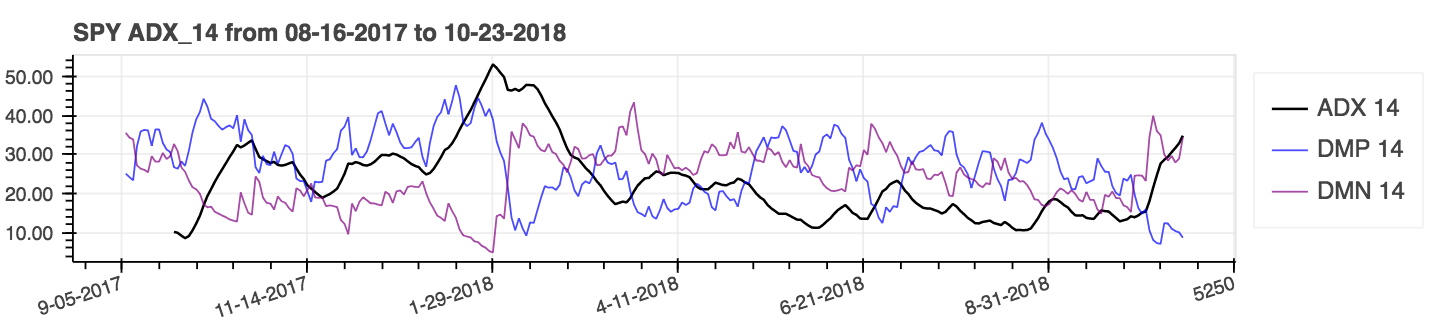

lookahead=False لتعطيل التركيز وإزالة تسرب البيانات المحتمل.| متوسط مؤشر حركة الاتجاه (ADX) |

|---|

|

| متوسط النطاق الحقيقي (ATR) |

|---|

|

| حجم الموازن (obv) |

|---|

|

مقاييس الأداء هي إضافة جديدة إلى الحزمة ، وبالتالي فمن المحتمل أن تكون غير موثوقة. استخدم على مسؤوليتك الخاصة. هذه المقاييس تُرجع تعويمًا وليست جزءًا من امتداد DataFrame . يطلق عليهم الطريق القياسي. على سبيل المثال:

import pandas_ta as ta

result = ta . cagr ( df . close ) من أجل التكامل الأسهل مع محفظة VectorBT من طريقة from_signals ، تم استبدال طريقة ta.trend_return بطريقة ta.tsignals لتبسيط توليد إشارات التداول. للحصول على مثال شامل ، راجع مثال Jupyter Notebook VectorBT Backtest مع Pandas TA في دليل الأمثلة.

import pandas as pd

import pandas_ta as ta

import vectorbt as vbt

df = pd . DataFrame (). ta . ticker ( "AAPL" ) # requires 'yfinance' installed

# Create the "Golden Cross"

df [ "GC" ] = df . ta . sma ( 50 , append = True ) > df . ta . sma ( 200 , append = True )

# Create boolean Signals(TS_Entries, TS_Exits) for vectorbt

golden = df . ta . tsignals ( df . GC , asbool = True , append = True )

# Sanity Check (Ensure data exists)

print ( df )

# Create the Signals Portfolio

pf = vbt . Portfolio . from_signals ( df . close , entries = golden . TS_Entries , exits = golden . TS_Exits , freq = "D" , init_cash = 100_000 , fees = 0.0025 , slippage = 0.0025 )

# Print Portfolio Stats and Return Stats

print ( pf . stats ())

print ( pf . returns_stats ())mamode KWARG مع المزيد من الخيارات المتوسطة المتحركة مع وظيفة الأداة المساعدة المتوسطة المتحركة ta.ma() . من أجل البساطة ، جميع الخيارات هي متوسطات نقل مصدر واحد. هذا هو في المقام الأول فائدة داخلية تستخدمها المؤشرات التي لها mamode kwarg . ويشمل ذلك المؤشرات: Accbands ، AMAT ، AOBV ، ATR ، BBANDS ، BIAS ، EFI ، HILO ، KC ، NATR ، QQE ، RVI ، و THERMO ؛ لم تتغير معلمات mamode الافتراضية. ومع ذلك ، يمكن استخدام ta.ma() من قبل المستخدم أيضًا إذا لزم الأمر. لمزيد من المعلومات: help(ta.ma)to_utc ، لتحويل فهرس DataFrame إلى UTC. انظر: help(ta.to_utc) الآن كخاصية PANDAS TA DATAFRAME لتحويل فهرس DataFrame بسهولة إلى UTC. close > sma(close, 50) فإنها تُرجع الاتجاه ، وإدخالات التجارة والمخارج التجارية لهذا الاتجاه لجعلها متوافقة مع VectorBT عن طريق تعيين asbool=True للحصول على إدخالات التجارة المنطقية والخروج. انظر help(ta.tsignals) help(ta.alma) حساب التداول ، أو الصندوق. انظر help(ta.drawdown)help(ta.cdl_pattern)help(ta.cdl_z)help(ta.cti)help(ta.xsignals)help(ta.dm)help(ta.ebsw)help(ta.jma)help(ta.kvo)help(ta.stc)help(ta.squeeze_pro)df.ta.strategy() لأسباب الأداء. انظر help(ta.td_seq)help(ta.tos_stdevall)help(ta.vhf) mamode المعاد تسميتها إلى mode . انظر help(ta.accbands) .mamode مع " RMA " الافتراضية ونفس خيارات mamode مثل TradingView. حجة جديدة lensig بحيث تتصرف مثل مؤشر ADX المدمج في TradingView. انظر help(ta.adx) .drift المضافة وأسماء الأعمدة الوصفية.mamode الافتراضي الآن " RMA " ومع نفس خيارات mamode مثل TradingView. انظر help(ta.atr) .ddoff للسيطرة على درجات الحرية. وشملت أيضا BB في المئة (BBP) كعمود نهائي. الافتراضي هو 0. انظر help(ta.bbands) .ln لاستخدام اللوغاريتم الطبيعي (صواب) بدلاً من اللوغاريتم القياسي (خطأ). الافتراضي كاذب. انظر help(ta.chop) .tvmode مع True الافتراضي. عندما يكون tvmode=False ، ينفذ CKSP "المتداول الفني الجديد" مع القيم الافتراضية. انظر help(ta.cksp) .talib إصدار TA Lib وإذا تم تثبيت TA LIB. الافتراضي صحيح. انظر help(ta.cmo) .strict إذا كانت السلسلة تتناقص باستمرار على length الفترة مع حساب أسرع. الافتراضي: False . كما تمت إضافة حجة percent مع الافتراضي لا شيء. انظر help(ta.decreasing) .strict إذا كانت السلسلة تزداد باستمرار على length الفترة مع حساب أسرع. الافتراضي: False . كما تمت إضافة حجة percent مع الافتراضي لا شيء. انظر help(ta.increasing) .help(ta.kvo) .as_strided أو طريقة sliding_window_view الأحدث. يجب أن يحل هذا المشكلات مع Google Colab وتأخر تحديثات التبعية وكذلك تبعيات TensorFlow كما تمت مناقشته في القضايا رقم 285 و #329.asmode كإصدار من MACD. الافتراضي كاذب. انظر help(ta.macd) .sar TradingView. حجة جديدة af0 لتهيئة عامل التسارع. انظر help(ta.psar) .mamode كخيار. الافتراضي هو SMA لمطابقة TA LIB. انظر help(ta.ppo) .signal مضافة مع الافتراضي 13 و MA mamode MAMODE مع EMA الافتراضي كوسائط. انظر help(ta.tsi) .help(ta.vp) .help(ta.vwma) .anchor . الافتراضي: "D" لـ "Daily". انظر مرورات الأوقات المعارضة الأسماء المستعارة لخيارات إضافية. يتطلب فهرس DataFrame ليكون dateTimeIndex. انظر help(ta.vwap) .help(ta.vwma) .Z_length إلى ZS_length . انظر help(ta.zscore) .الأصلي ta-lib | TradingView | سييرا تشارت | MQL5 | FM Labs | برو كود حقيقي | المستخدم 42

هل تشعر بالسخاء ، مثل الحزمة أو تريد رؤيتها تصبح أكثر حزمة ناضجة؟