GGS

1.0.0

Greedy Gaussian Segmentation (GGS) is a Python solver for efficiently segmenting multivariate time series data. For implementation details, please see our paper at http://stanford.edu/~boyd/papers/ggs.html.

The GGS Solver takes an n-by-T data matrix and breaks the T timestamps on an n-dimensional vector into segments over which the data is well explained as independent samples from a multivariate Gaussian distribution. It does so by formulating a covariance-regularized maximum likelihood problem and solving it using a greedy heuristic, with full details described in the paper.

git clone [email protected]:davidhallac/GGS.git

cd GGS

python helloworld.py

ggs.py is in the same directory as your new file, and then add the following code to the beginning of your script:from ggs import *

The GGS package has three main functions:

bps, objectives = GGS(data, Kmax, lamb)

Finds K breakpoints in the data for a given regularization parameter lambda

Inputs

data - a n-by-T data matrix, with T timestamps of an n-dimensional vector

Kmax - the number of breakpoints to find

lamb - regularization parameter for the regularized covariance

Returns

bps - List of lists, where element i of the larger list is the set of breakpoints found at K = i in the GGS algorithm

objectives - List of the objective values at each intermediate step (for K = 0 to Kmax)

meancovs = GGSMeanCov(data, breakpoints, lamb)

Finds the means and regularized covariances of each segment, given a set of breakpoints.

Inputs

data - a n-by-T data matrix, with T timestamps of an n-dimensional vector

breakpoints - a list of breakpoint locations

lamb - regularization parameter for the regularized covariance

Returns

meancovs - a list of (mean, covariance) tuples for each segment in the data

cvResults = GGSCrossVal(data, Kmax=25, lambList = [0.1, 1, 10])

Runs 10-fold cross validation, and returns the train and test set likelihood for every (K, lambda) pair up to Kmax

Inputs

data - a n-by-T data matrix, with T timestamps of an n-dimensional vector

Kmax - the maximum number of breakpoints to run GGS on

lambList - a list of regularization parameters to test

Returns

cvResults - list of (lamb, ([TrainLL],[TestLL])) tuples for each regularization parameter in lambList. Here, TrainLL and TestLL are the average per-sample log-likelihood across the 10 folds of cross-validation for all K's from 0 to Kmax

Additional optional parameters (for all three functions above):

features = [] - select a certain subset of columns in the data to operate on

verbose = False - Print intermediate steps when running the algorithm

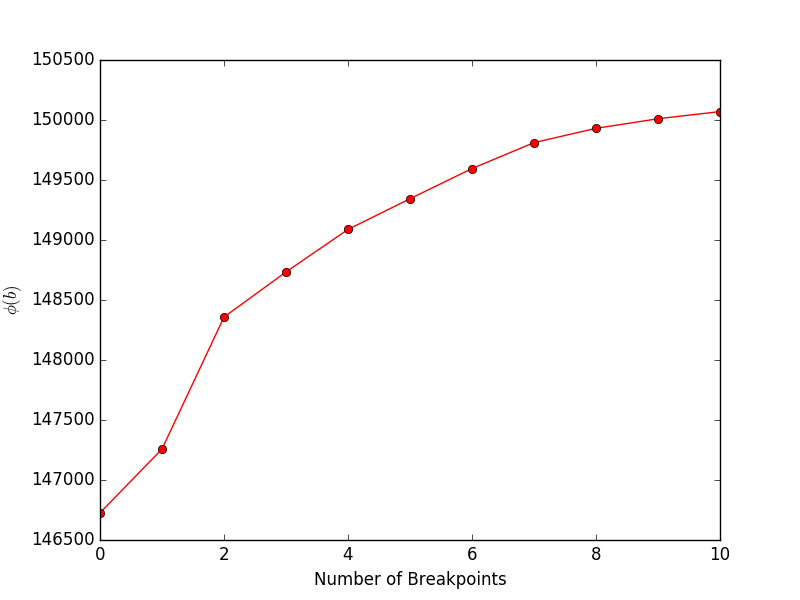

Running financeExample.py will yield the following plot, showing the objective (Equation 4 in the paper) vs. the number of breakpoints:

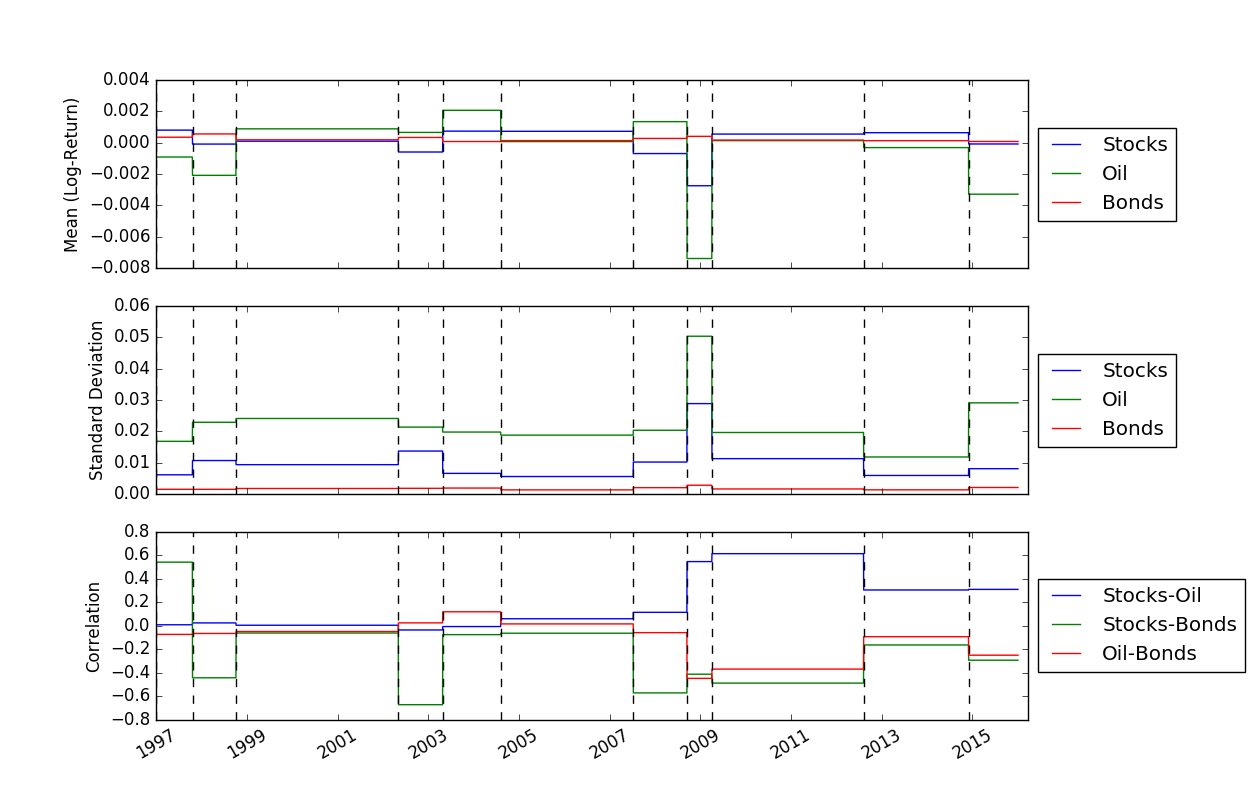

Once we have solved for the locations of the breakpoints, we can use the FindMeanCovs() function to find the means and covariances of each segment. In the example in helloworld.py, plotting the means, variances, and covariances of the three signals yields:

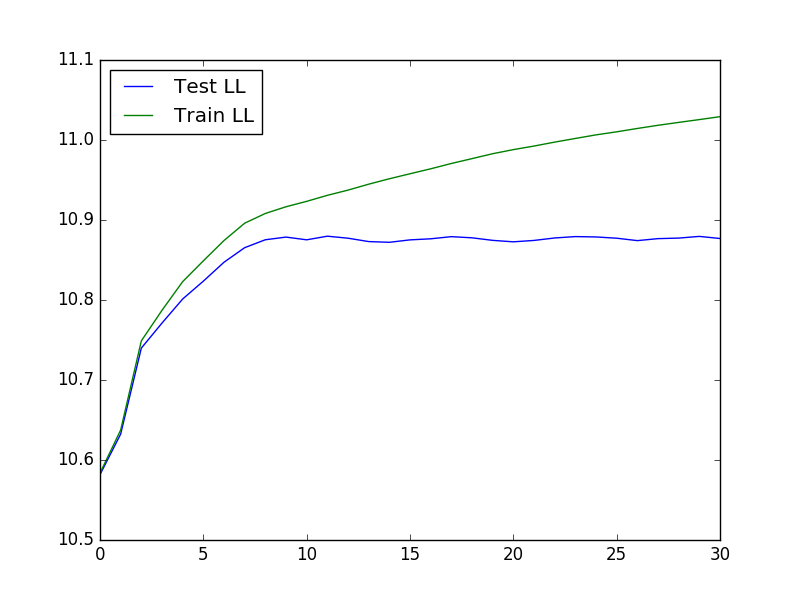

To run cross-validation, which can be useful in determining optimal values of K and lambda, we can use the following code to load the data, run the cross-validation, and then plot the test and train likelihood:

from ggs import *

import numpy as np

import matplotlib.pyplot as plt

filename = "Returns.txt"

data = np.genfromtxt(filename,delimiter=' ')

feats = [0,3,7]

#Run cross-validaton up to Kmax = 30, at lambda = 1e-4

maxBreaks = 30

lls = GGSCrossVal(data, Kmax=maxBreaks, lambList = [1e-4], features = feats, verbose = False)

trainLikelihood = lls[0][1][0]

testLikelihood = lls[0][1][1]

plt.plot(range(maxBreaks+1), testLikelihood)

plt.plot(range(maxBreaks+1), trainLikelihood)

plt.legend(['Test LL','Train LL'], loc='best')

plt.show()

The resulting plot looks like:

Greedy Gaussian Segmentation of Time Series Data -- D. Hallac, P. Nystrup, and S. Boyd

David Hallac, Peter Nystrup, and Stephen Boyd.